Introduction

The aim of this post is to give the updated baseline portfolio weights of the Polar Star Diversified Commodity Fund for the fourth quarter of 2020. We employ the Black-Litterman methodology to tilt the allocations slighlty toward the underlying fund the greater return expectations and confidence. For more details on the process please see this link as well as other referenes therein.

Baseline Weights

To obtain baseline weights, we perform a risk-adjusted return portfolio optimisation with the returns stream of the three underlying funds

- Polar Star Ltd

- Polar Star Specturm

- Polar Star Quantitataive

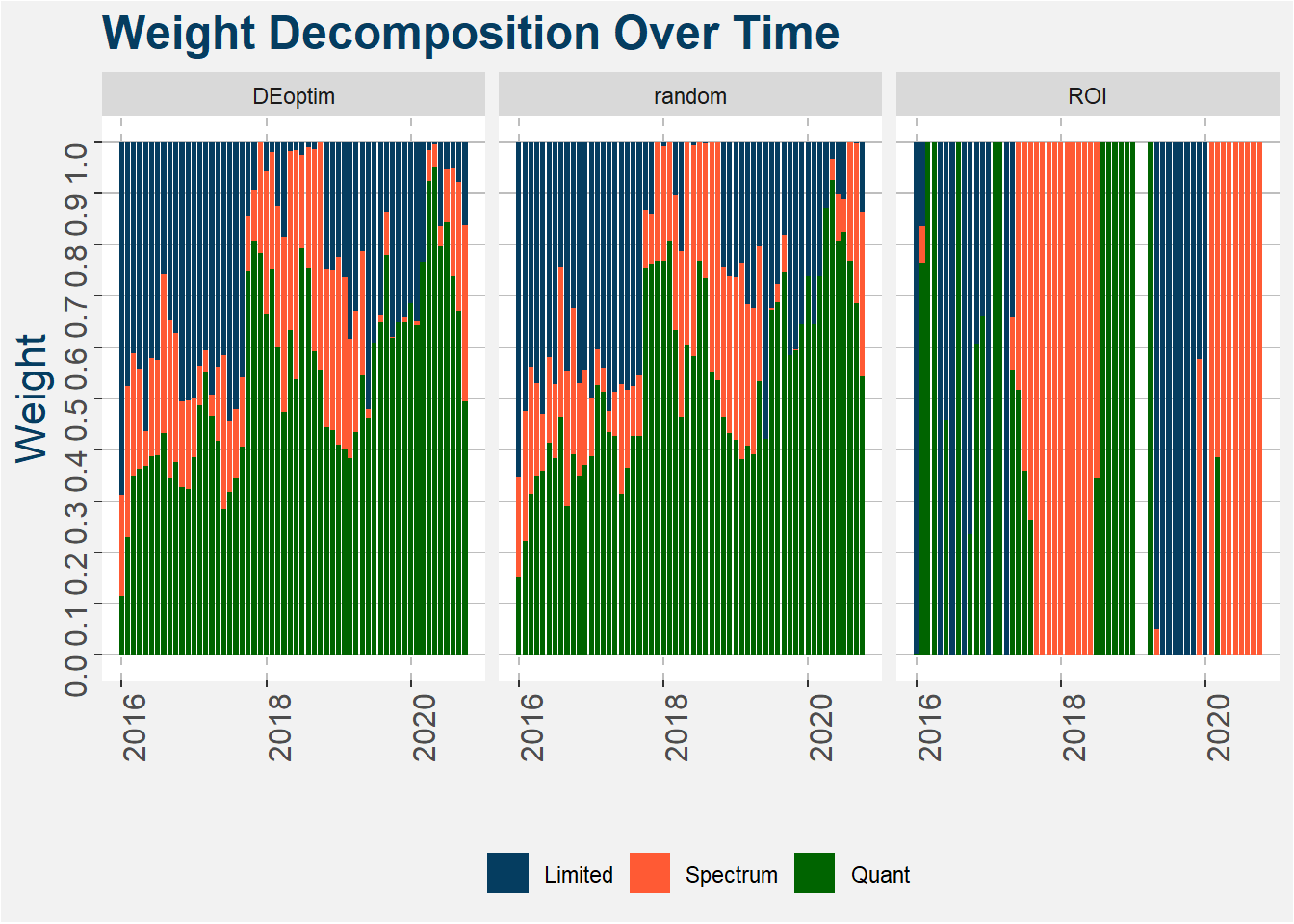

We use a training period of 12 months from which we determine the optimal portfolio in the following month. In previous calculations we used 12 months of returns with an expanding window to determine the optimal wights, here we use a 12 month rolling window. The evolution of the optimal weights is shown in the plot below for three different optimisation schemes. These are just numerical method used to determine the optimal weights. Notice that we have reduced the range of returns to start from 2015, this is done to place a greater emphasis on returns closer to the current regime.

As baseline weights we take the average of the optimised weights given by the table below. Here each columns from the ROI method as the baseline weights.

| fund | Average | DEoptim | ROI | random |

|---|---|---|---|---|

| Limited | 0.29 | 0.278 | 0.302 | 0.277 |

| Spectrum | 0.25 | 0.182 | 0.392 | 0.179 |

| Quant | 0.46 | 0.540 | 0.306 | 0.544 |

Weight Change vs Return Forecast

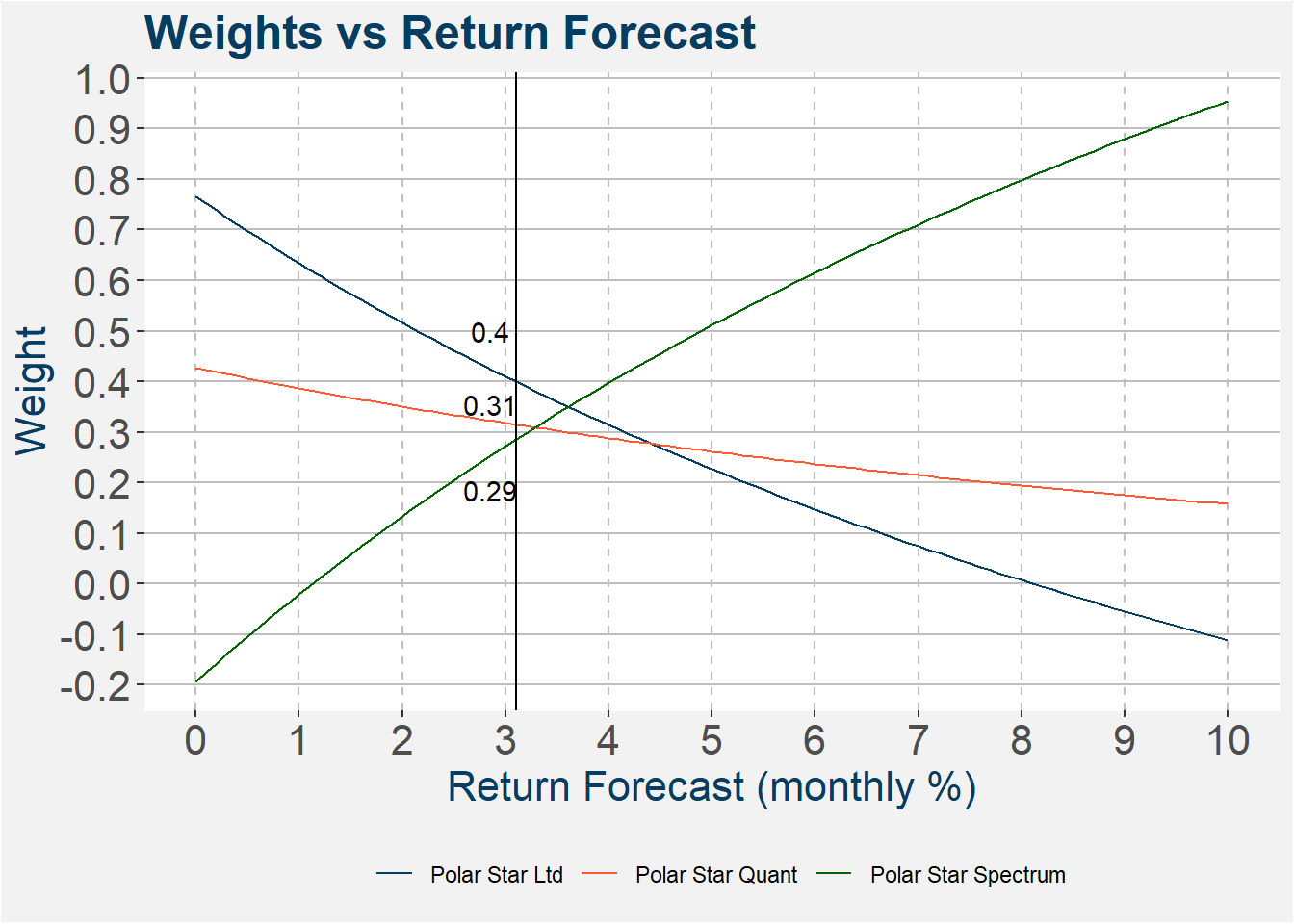

Here we fix the return forecasts of Polar Star Quantitative and Polar Star Limited and let the return forecast of Polar Star Spectrum vary from 0 through 10%. Notice that the numbers shown in the image below take the eighteen month forecasts and generate a monthly aggregate number from it (cumulative return). Notice that as the return forecast increases so the weight allocated to Polar Star Spectrum increases.

The table below shows the weights after tilting the allocations slightly according to the outline above.

| Fund | Return Forecast (monthly) | Weight |

|---|---|---|

| Polar Star Ltd | 0.031 | 0.400 |

| Polar Star Spectrum | 0.031 | 0.285 |

| Polar Star Quant | 0.031 | 0.315 |

Remarks

The final return projections and associated confidence levels have to be finilised by the portfolio managers of each of the underlying funds.